Deep Dive: Solana DeFi - March 2026

Deep Dive: Solana DeFi - March 2026 s

Note: Below is the text-accessible version of this post for visually impaired readers.

Syndica Deep Dive: Solana DeFi - March 2026

Part I Solana Spot DEXes

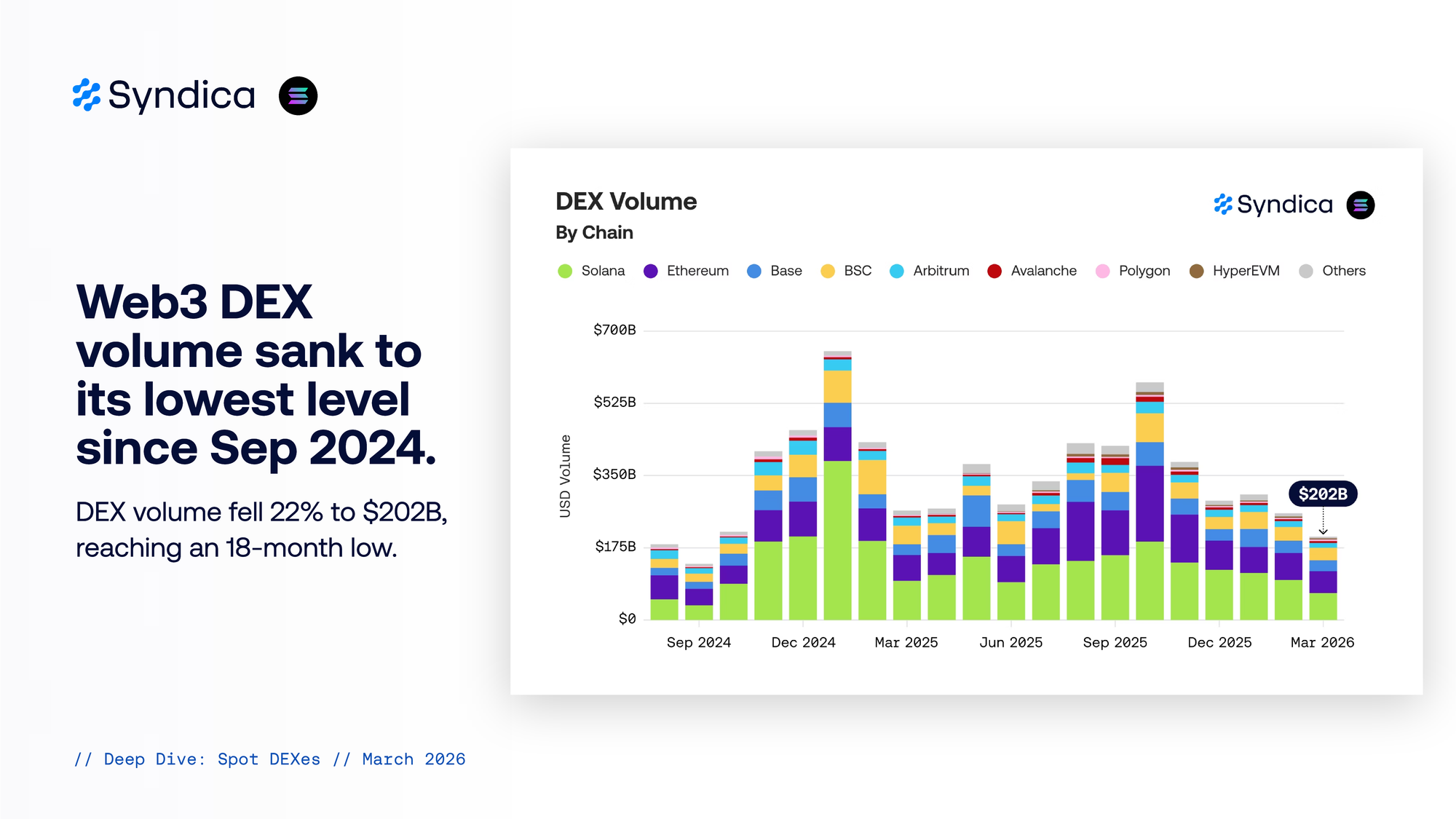

Web3 DEX volume sank to its lowest level since Sep 2024.

DEX volume fell 22% to $202B, reaching an 18-month low.

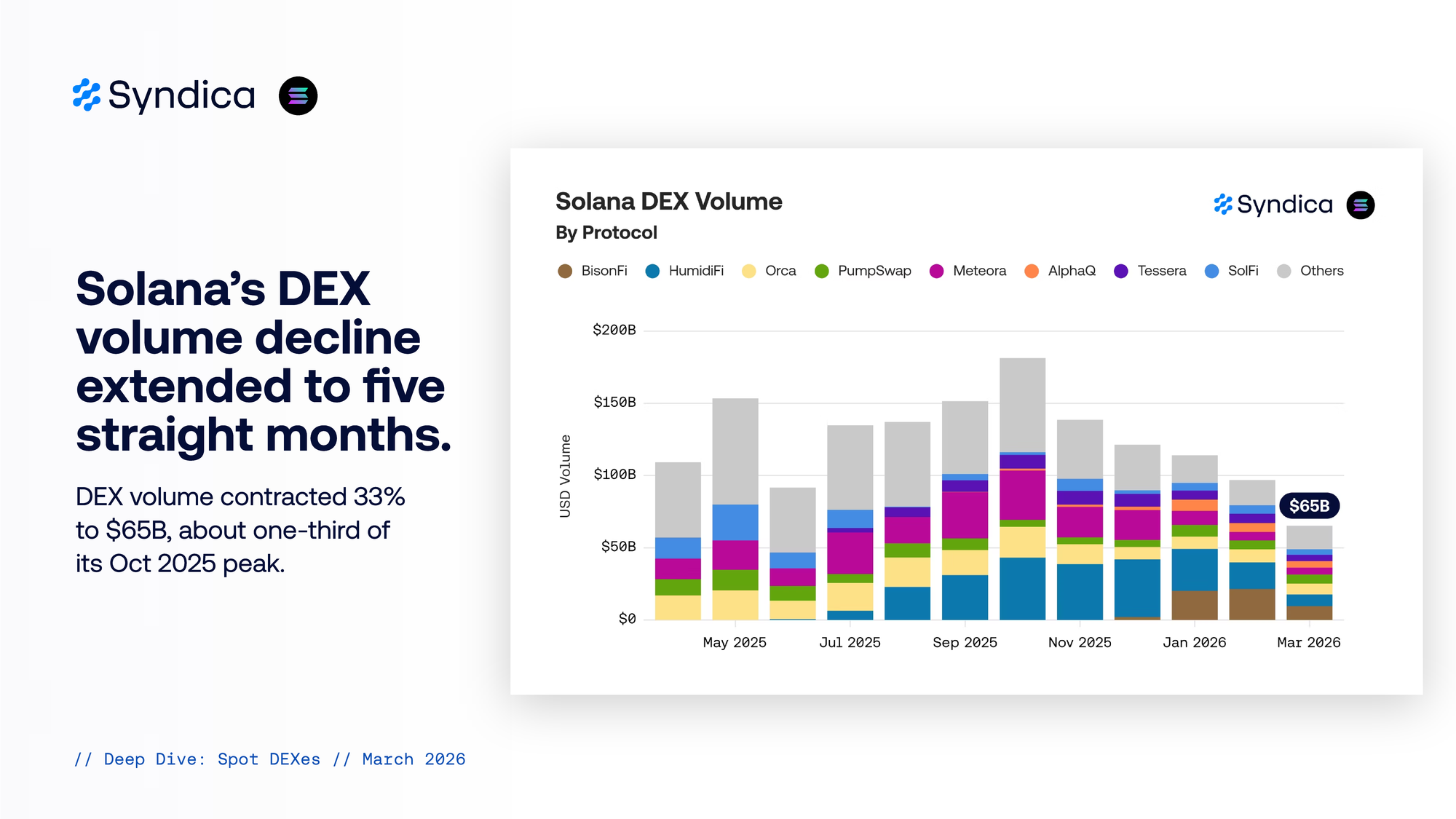

Solana’s DEX volume decline extended to five straight months.

DEX volume contracted 33% to $65B, about one-third of its Oct 2025 peak.

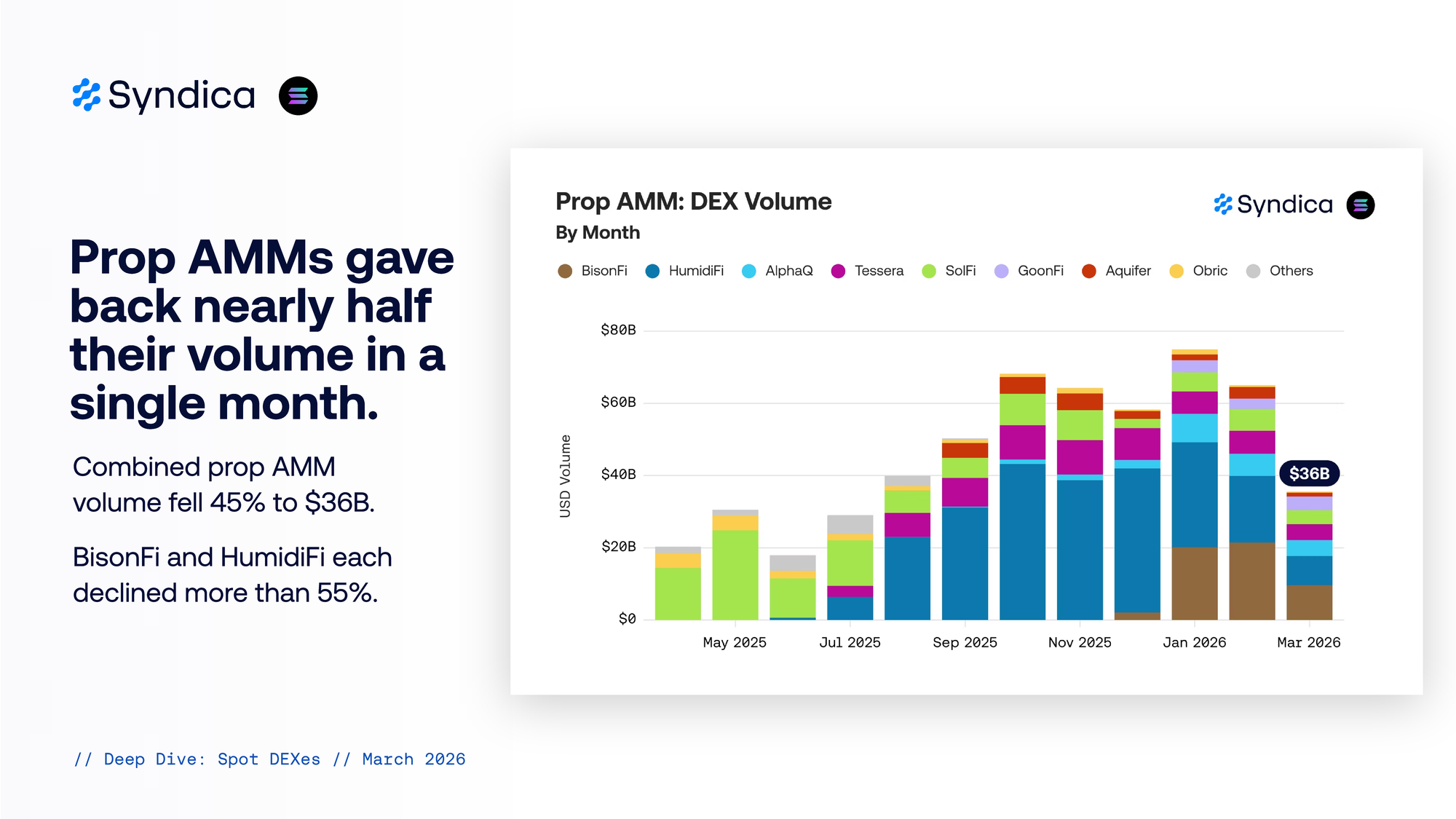

Prop AMMs gave back nearly half their volume in a single month.

Combined prop AMM volume fell 45% to $36B. BisonFi and HumidiFi each declined more than 55%.

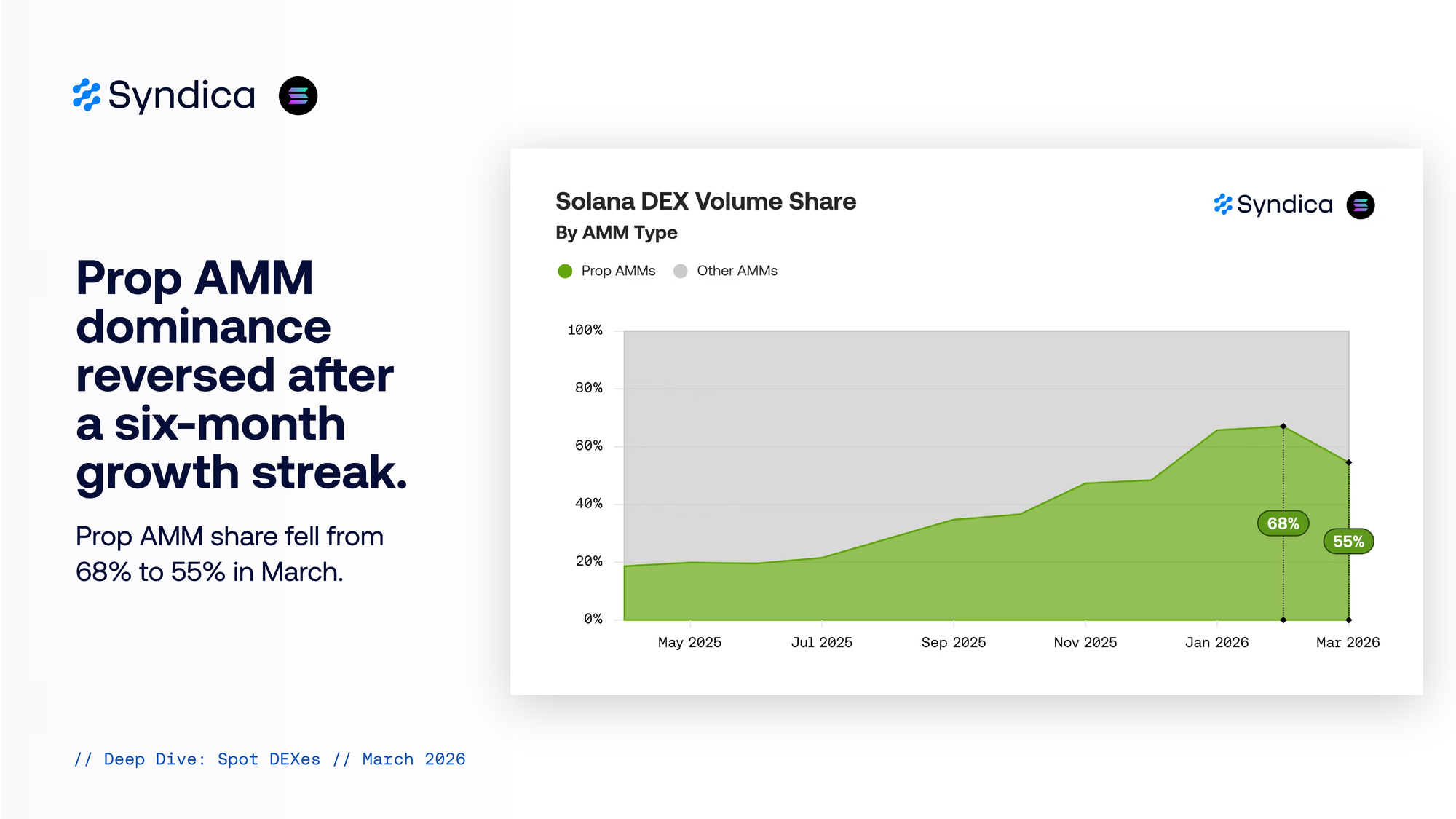

Prop AMM dominance reversed after a six-month growth streak.

Prop AMM share fell from 68% to 55% in March.

Part II Solana Lending & Borrowing

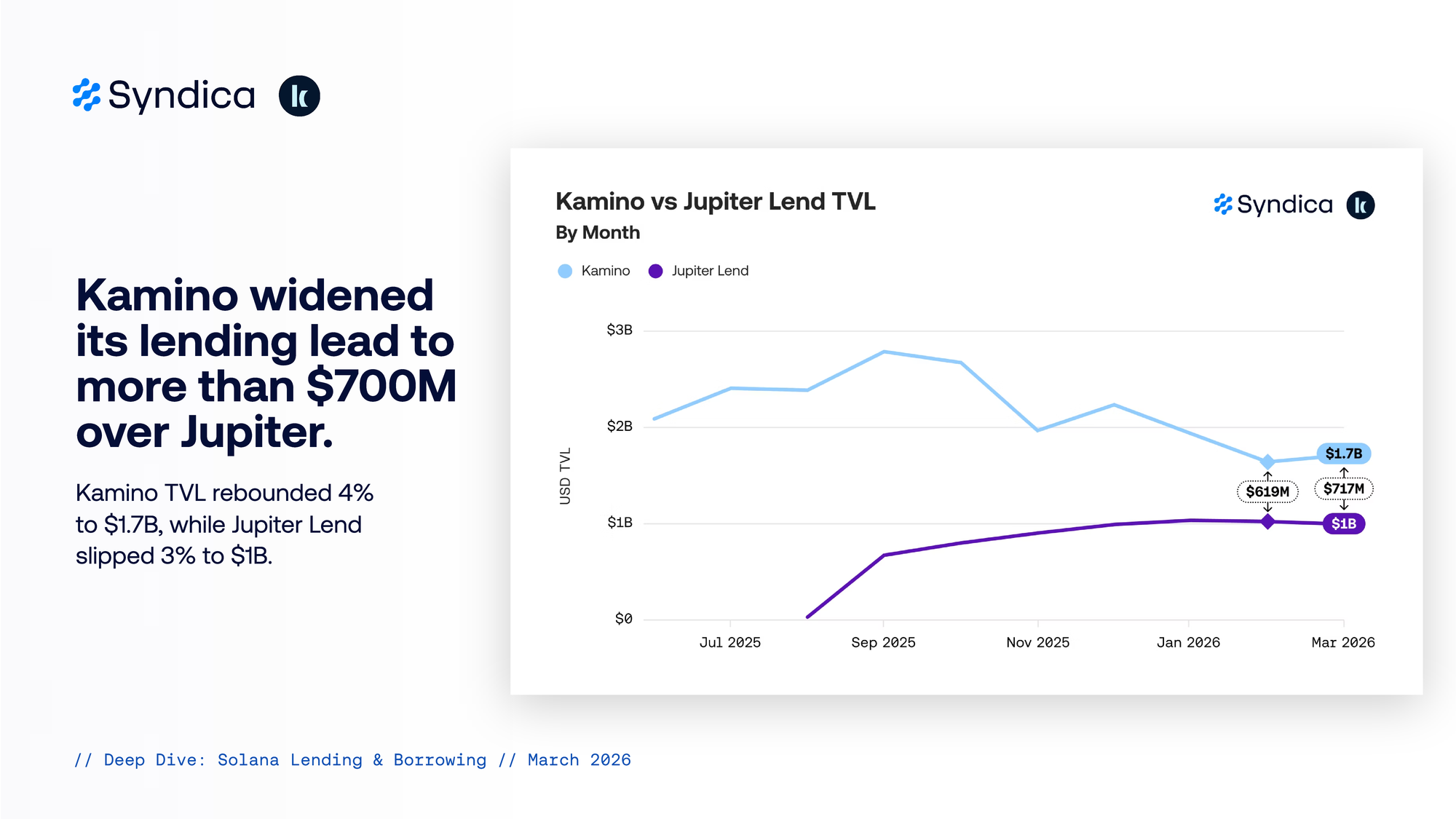

Kamino widened its lending lead to more than $700M over Jupiter.

Kamino TVL rebounded 4% to $1.7B, while Jupiter Lend slipped 3% to $1B.

Part III Solana Pegged Assets

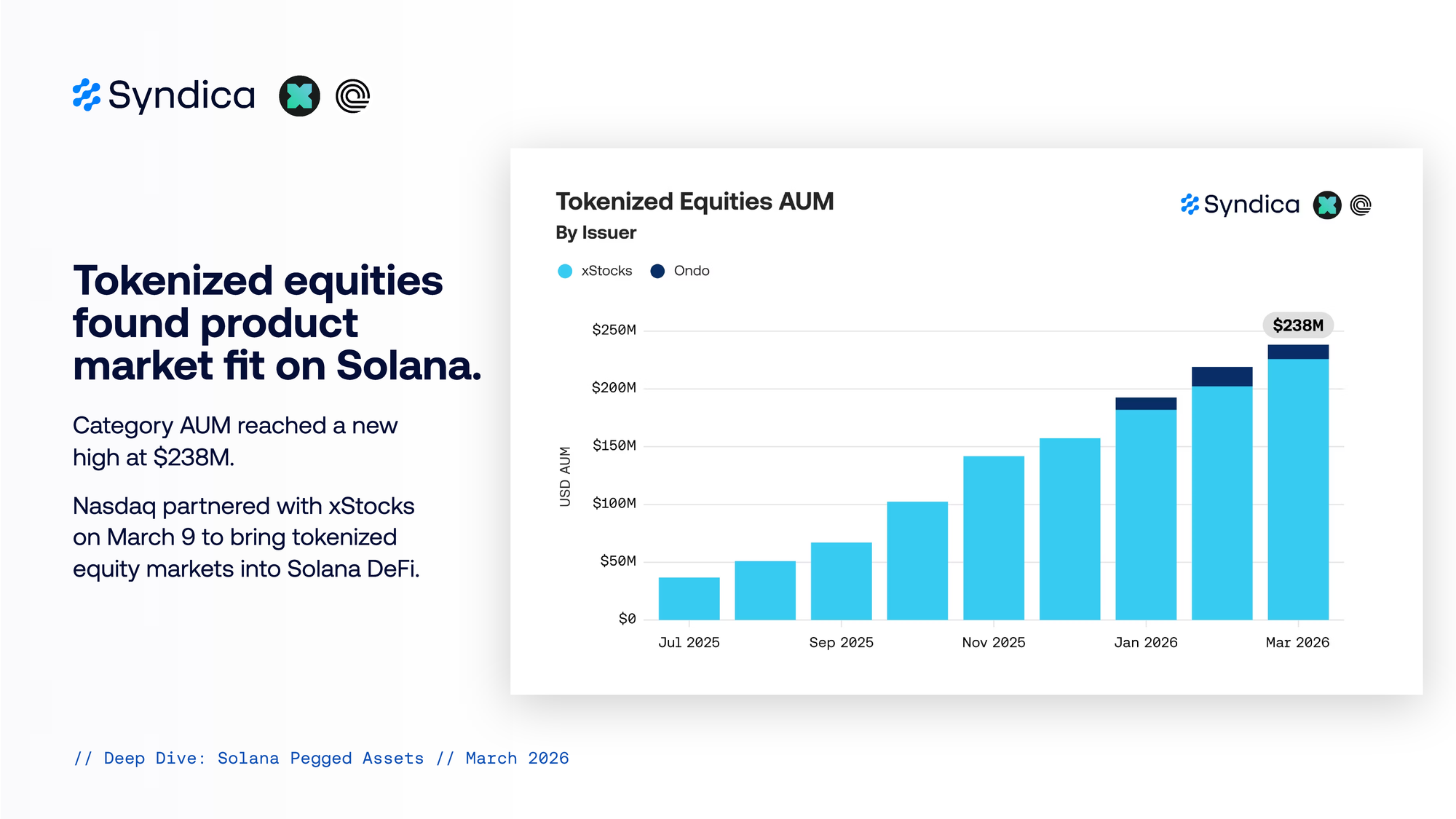

Tokenized equities found product market fit on Solana.

Category AUM reached a new high at $238M. Nasdaq partnered with xStocks on March 9 to bring tokenized equity markets into Solana DeFi.

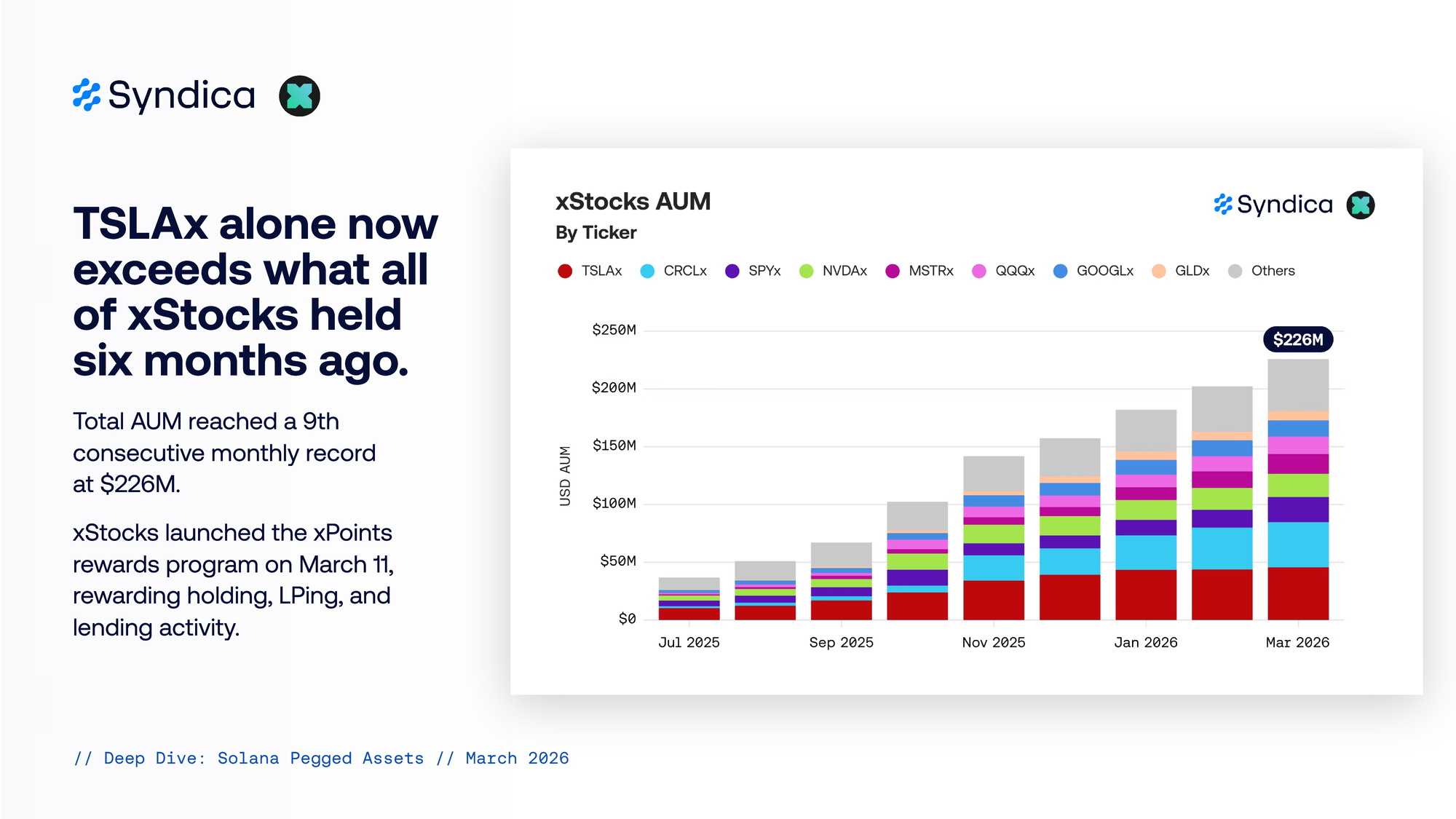

TSLAx alone now exceeds what all of xStocks held six months ago.

Total AUM reached a 9th consecutive monthly record at $226M. xStocks launched the xPoints rewards program on March 11, rewarding holding, LPing, and lending activity.

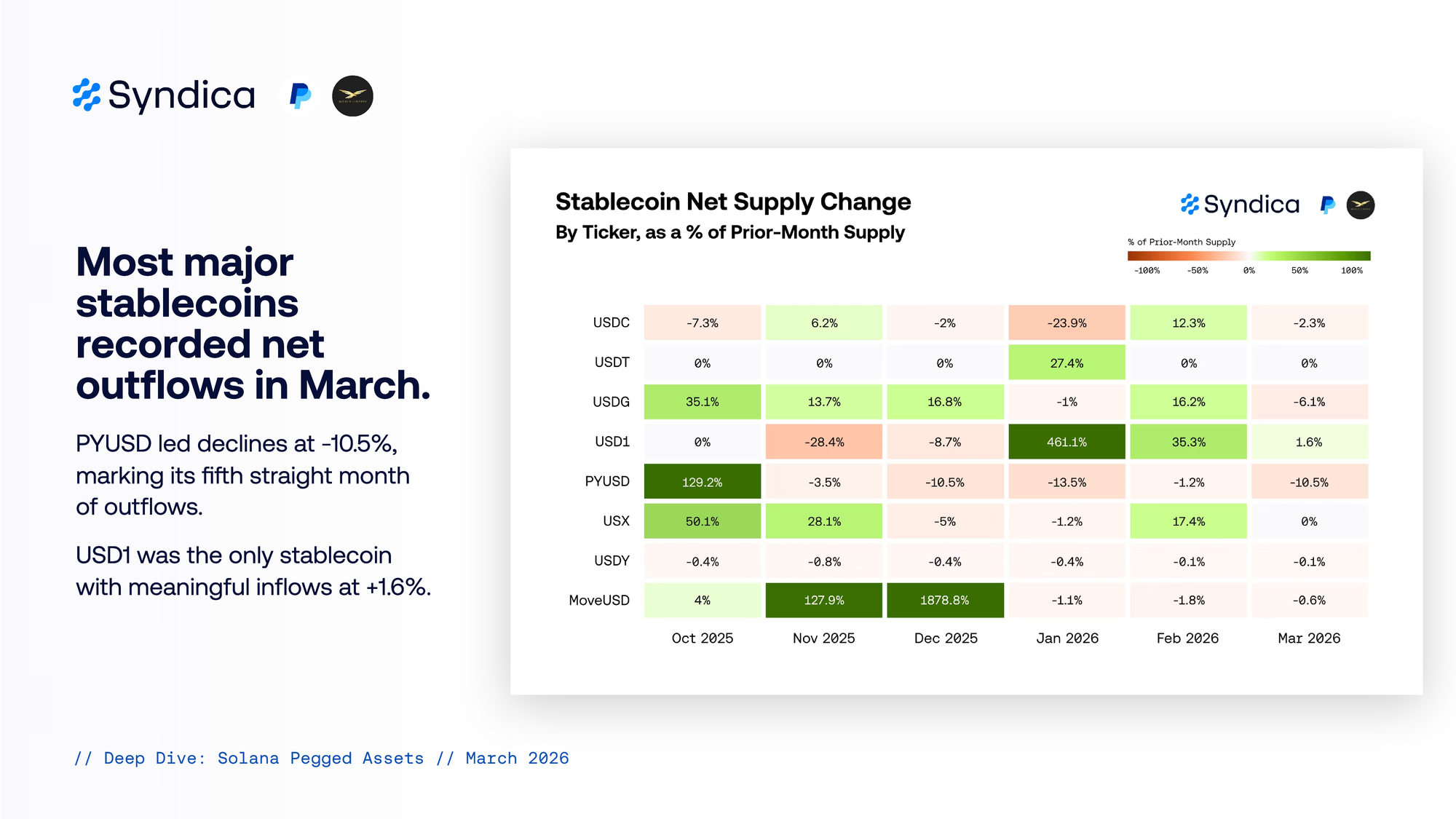

Most major stablecoins recorded net outflows in March.

PYUSD led declines at -10.5%, marking its fifth straight month of outflows. USD1 was the only stablecoin with meaningful inflows at +1.6%.

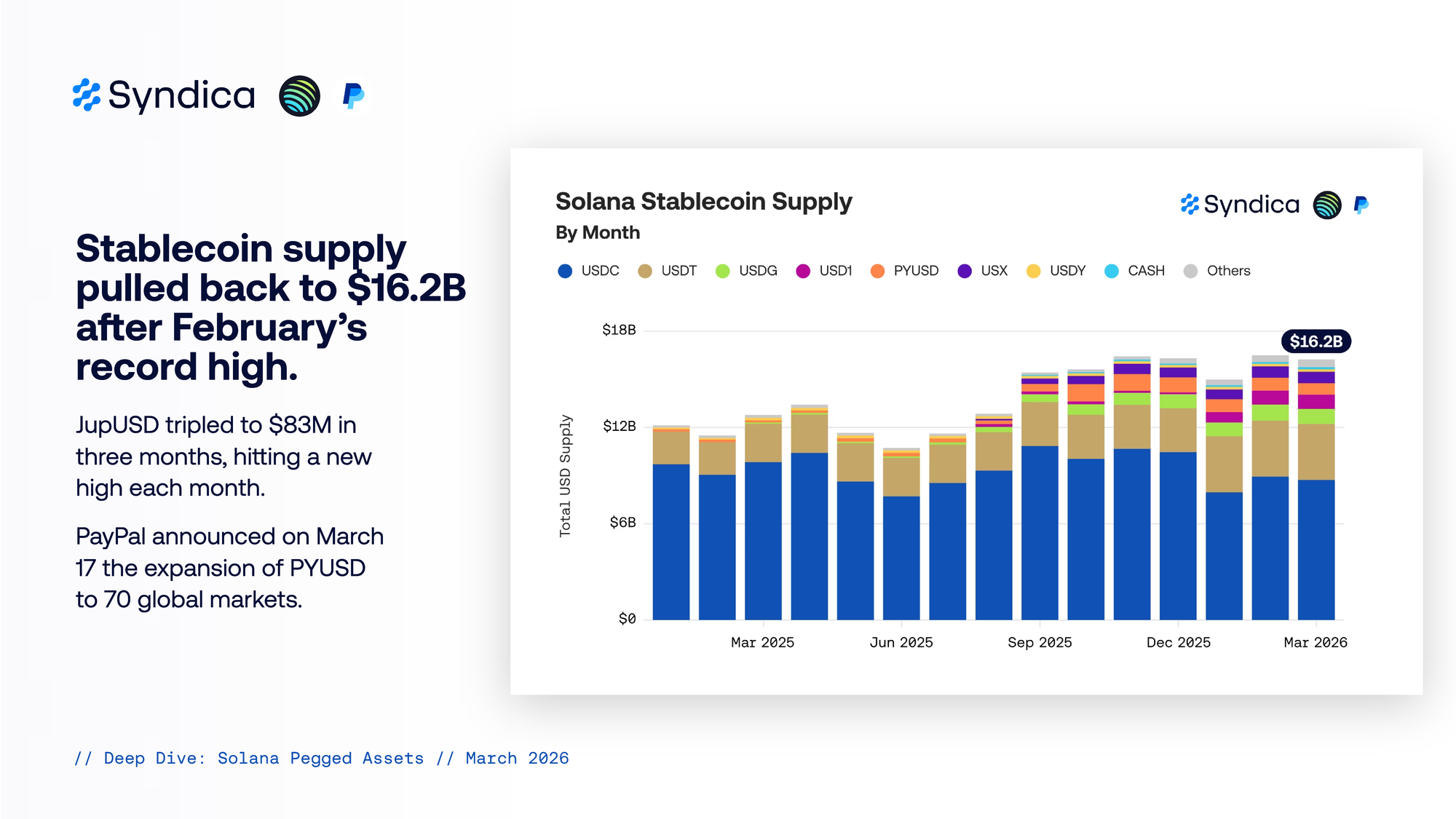

Stablecoin supply pulled back to $16.2B after February’s record high.

JupUSD tripled to $83M in three months, hitting a new high each month. PayPal announced on March 17 the expansion of PYUSD to 70 global markets.

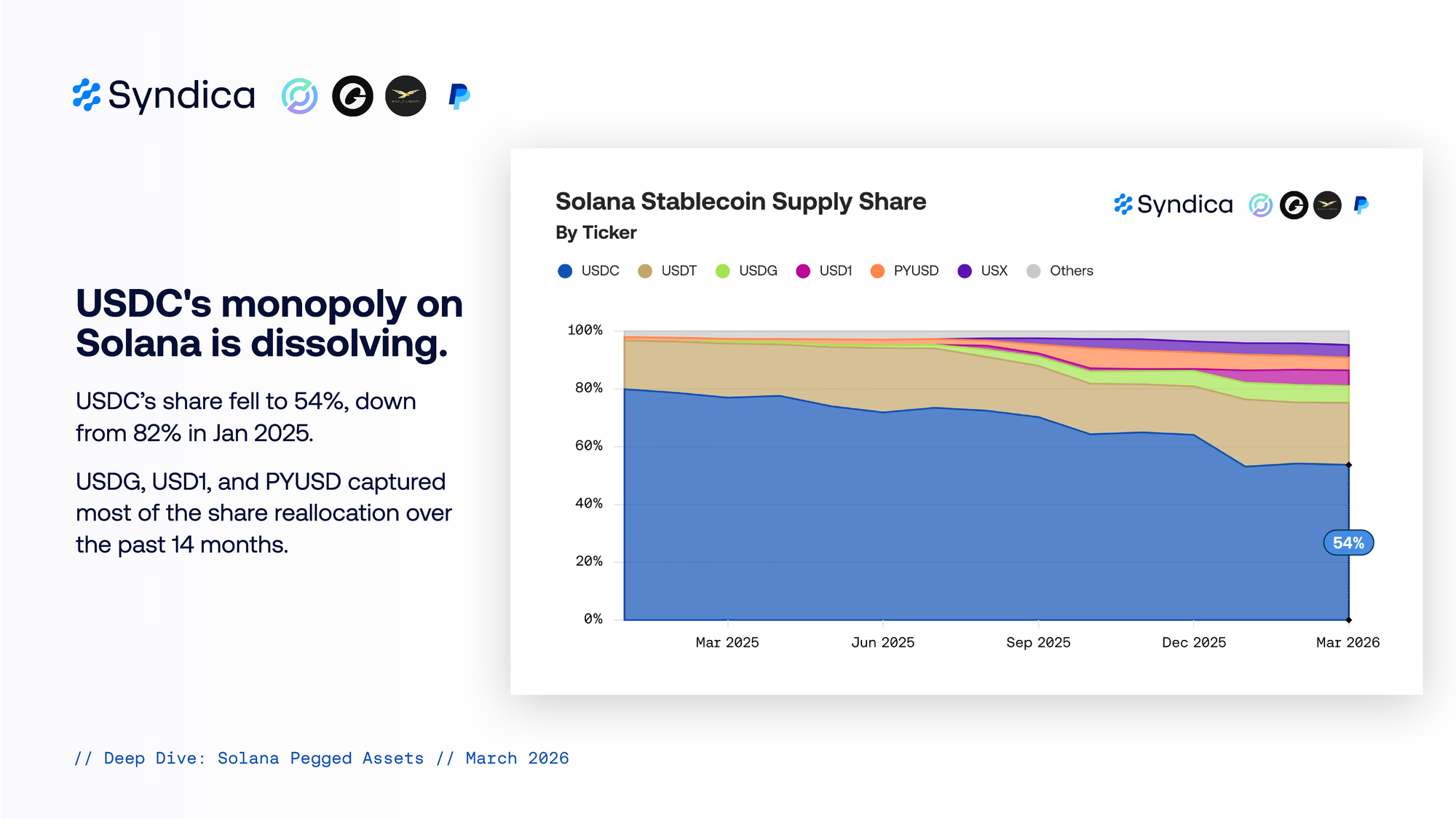

USDC's monopoly on Solana is dissolving.

USDC’s share fell to 54%, down from 82% in Jan 2025. USDG, USD1, and PYUSD captured most of the share reallocation over the past 14 months.

USDC accounted for 83% of transfers on just 54% of supply.

The gap between supply share and transfer share reinforced USDC's role in settlement and DeFi routing. Solana’s stablecoin transfer volume fell 31% to $667B from February's all-time high.

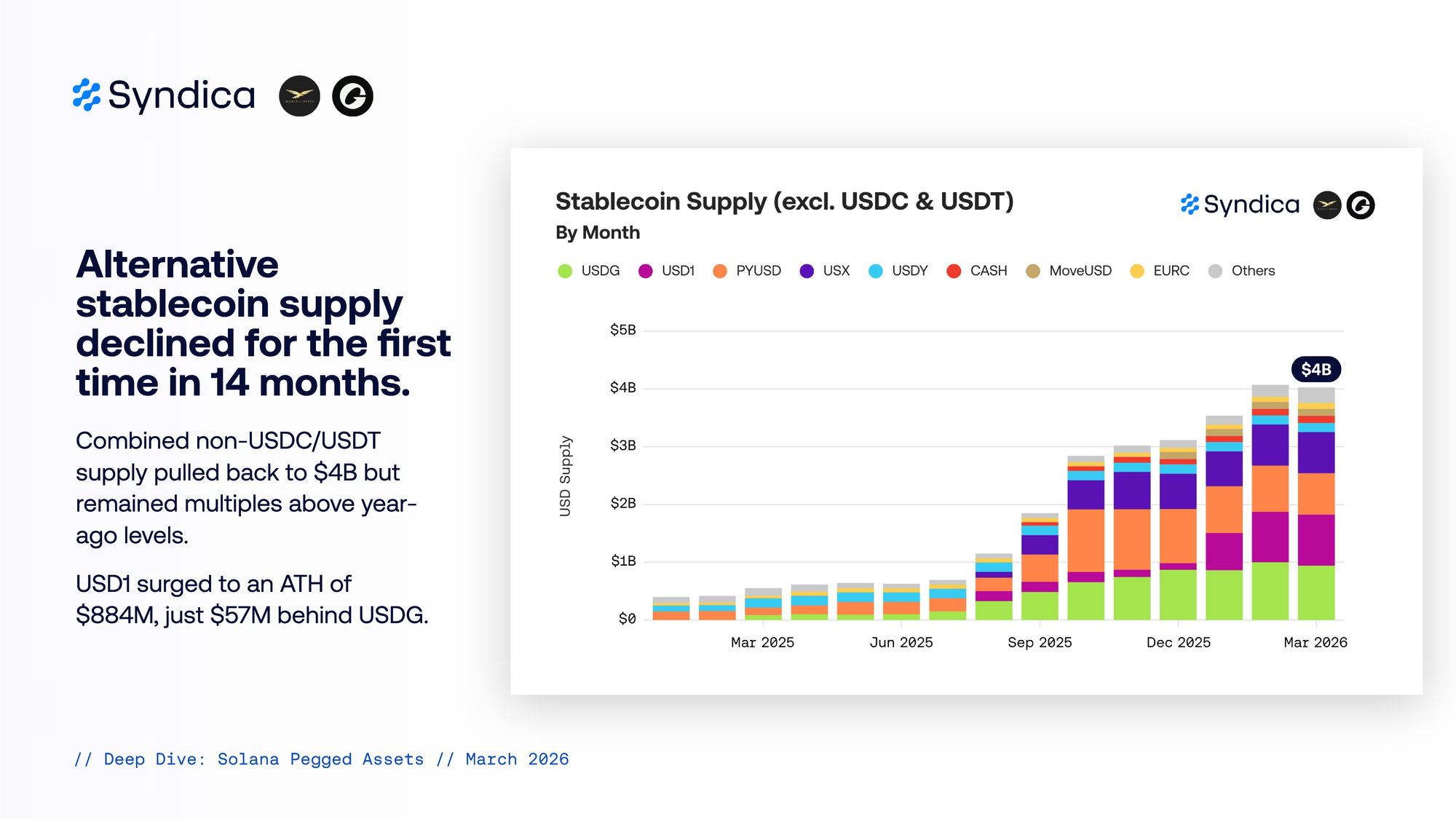

Alternative stablecoin supply declined for the first time in 14 months.

Combined non-USDC/USDT supply pulled back to $4B but remained multiples above year-ago levels. USD1 surged to an ATH of $884M, just $57M behind USDG.

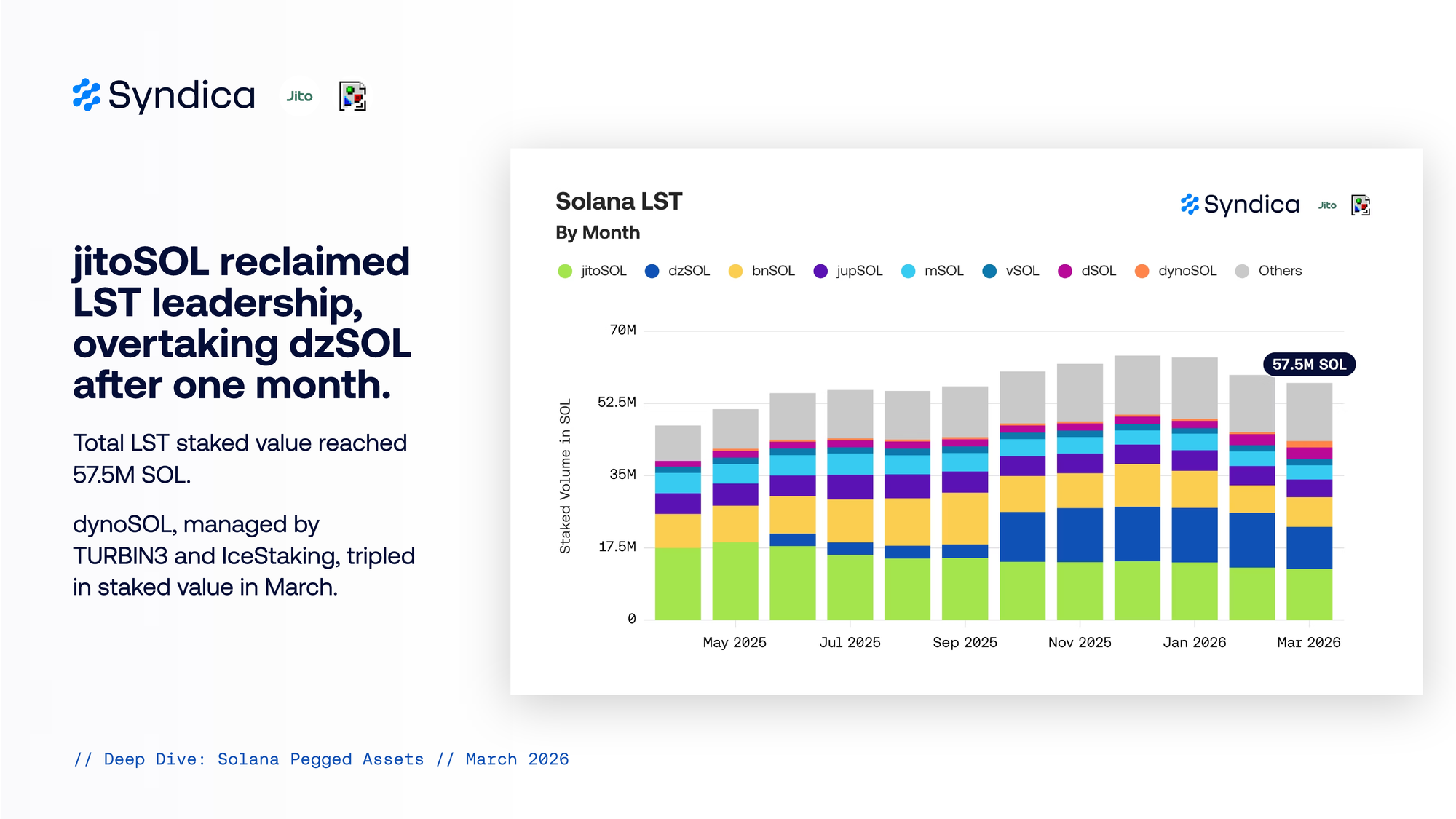

jitoSOL reclaimed LST leadership, overtaking dzSOL after one month.

Total LST staked value reached 57.5M SOL. dynoSOL, managed by TURBIN3 and IceStaking, tripled in staked value in March.

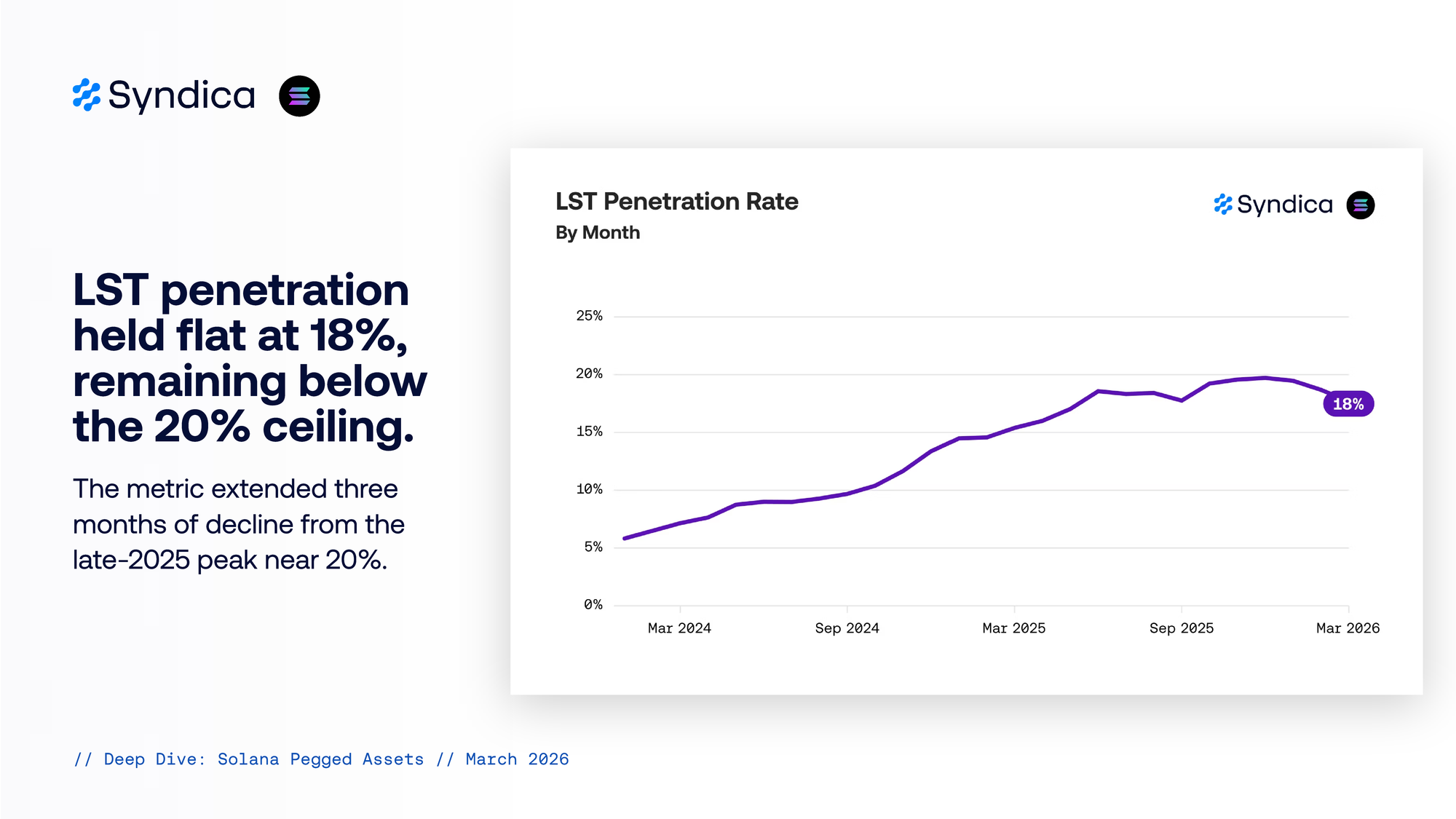

LST penetration held flat at 18%, remaining below the 20% ceiling.

The metric extended three months of decline from the late-2025 peak near 20%.

Part IV Token Launches

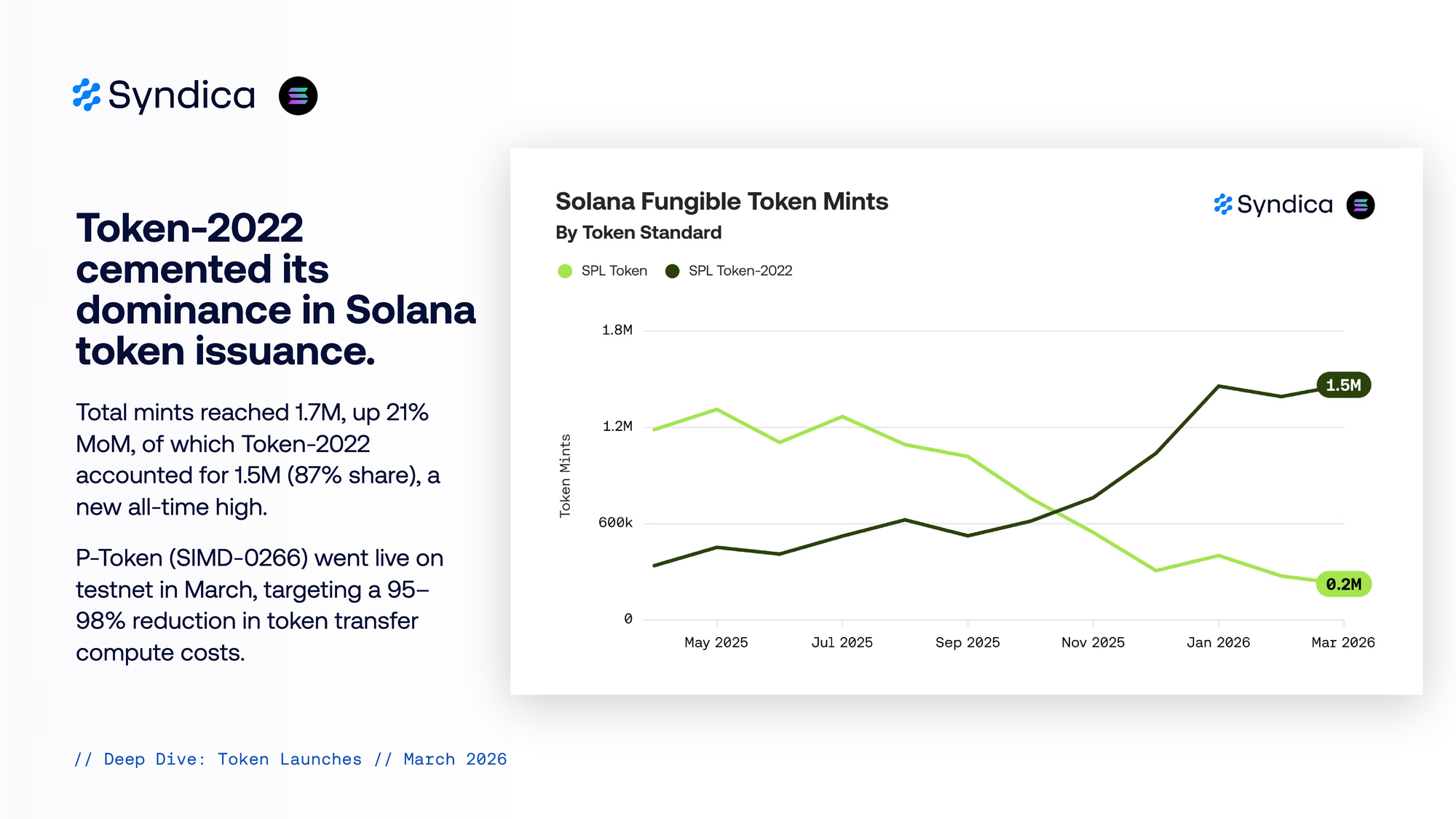

Token-2022 cemented its dominance in Solana token issuance.

Total mints reached 1.7M, up 21% MoM, of which Token-2022 accounted for 1.5M (87% share), a new all-time high. P-Token (SIMD-0266) went live on testnet in March, targeting a 95-98% reduction in token transfer compute costs.

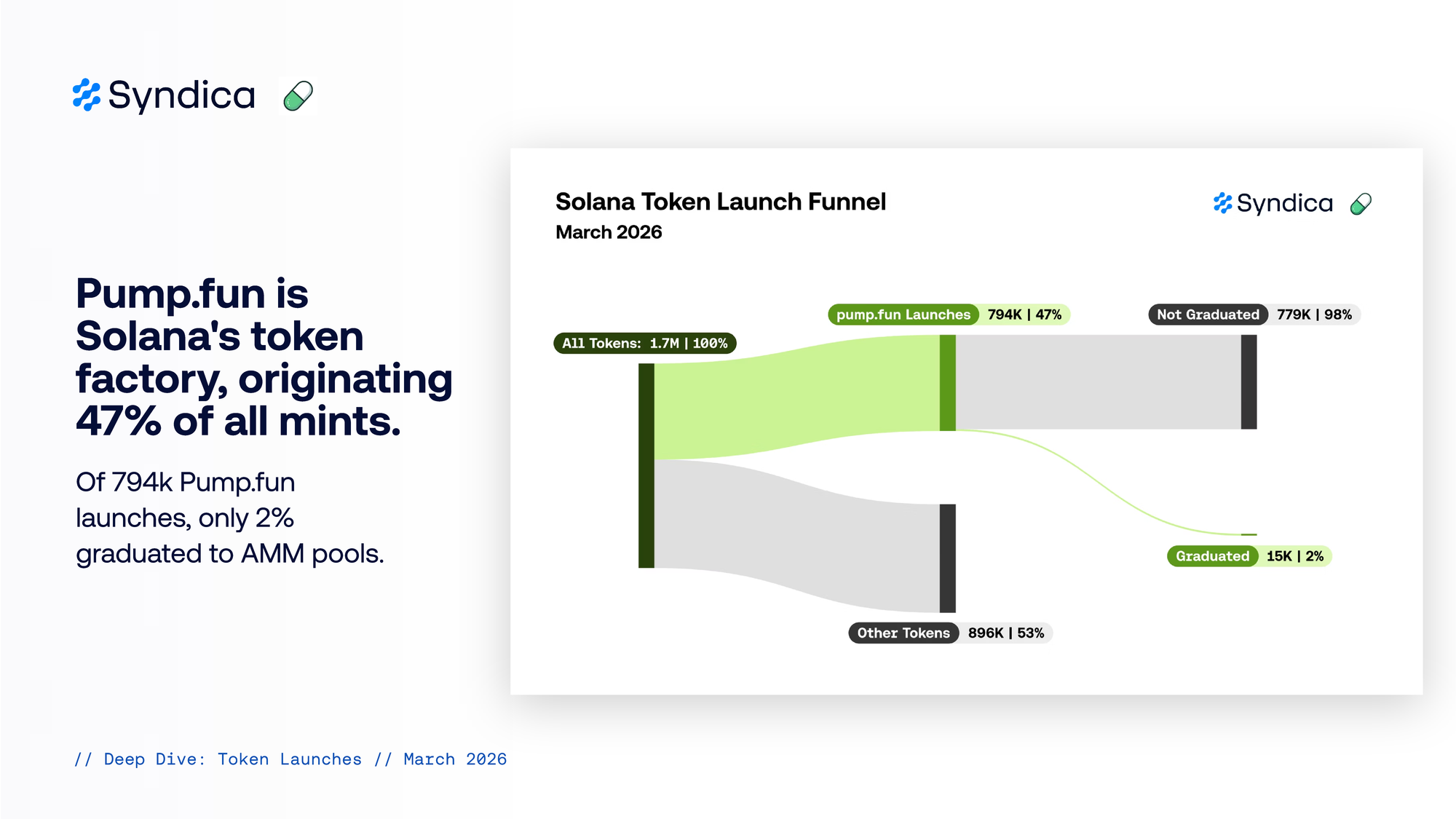

Pump.fun is Solana's token factory, originating 47% of all mints.

Of 794k Pump.fun launches, only 2% graduated to AMM pools.